Subscribe to stay informed, inspired and involved.

Subscribe

Sign up with your email

Introduction

On February 26, 2025, the European Commission released its proposed Omnibus package that streamlines the Corporate Sustainability Reporting Directive (CSRD), Corporate Sustainability Due Diligence Directive (CSDDD), and EU Taxonomy regulations.

The proposed Omnibus package comes two years after the CSRD was entered into force on January 5, 2023, and will significantly impact the eligibility, timing for reporting, and reporting requirements for nearly all companies. Many companies that fell within scope of the original CSRD have already published or were on the path to publish their first Sustainability Statements in 2025 and 2026. Many companies have invested significant time and resources into preparing for compliance.

Although the proposed changes are not yet final, companies that fell within the scope of the original CSRD should understand what the Omnibus package entails and how it may impact their CSRD preparedness strategy.

Why the Sustainability Omnibus Package?

Earlier this year, the Commission commited to simplify Europe’s new sustainability reporting and due diligence regimes. The simplification aims to address concerns about European economic stagnation and an overregulated business environment impeding European competitiveness, particularly for small and medium enterprises (SMEs) that do not have the resources for extensive reporting and due diligence. As part of the Competitive Compass, the Commission committed to reducing administrative burdens by at least 25% for all businesses and 35% for SMEs in the first half of 2025.

Additionally, as companies in the first wave of CSRD reporting completed their first Sustainability Statements, the Commission considered feedback and concerns such as the excessive time and cost for compliance, assurance burdens, and trickle-down effects in the value chain. The proposed Omnibus package is the Commission’s response.

Key changes to the CSRD

The proposals would significantly change the thresholds, timeline, and reporting requirements for the CSRD. The Commission estimates that nearly 80% of previously in-scope companies may now fall out of scope. Key changes highlighted below:

| Original CSRD | Omnibus Proposal | Key Takeaway | |

| Eligibility Requirements | |||

| Large undertakings (Wave 1 and 2) | Two of the following: • ≥ 500 (Wave 1) or ≥ 250 (Wave 2) employees • €50 million in net turnover • €25 million in assets |

≥ 1,000 employees AND at least one of the following: • €50 million in net turnover • €25 million in assets |

A higher threshold means nearly 80% of companies may fall out of scope of the CSRD. |

| Listed small and mid-size enterprises (SMEs) (Wave 3) | Two of the following: • ≥ 10 employees • ≥€900,000 net turnover (revenue) • ≥€450,000 total assets |

Not required to report under new thresholds | Listed SMEs are no longer subject to required CSRD reporting and “Value-chain cap” to prevent trickle down effects. |

| Third country undertakings | €150 million net turnover in the EU AND at least one of the following: • Branch with €40 million net turnover • Subsidiary that qualifies as a large undertaking (defined above) |

€450 million net turnover in the EU AND at least one of the following: • Branch with €50 million net turnover • Subsidiary that qualifies as a large undertaking (defined above) |

Due to the higher EU turnover threshold, fewer than 900 non-EU companies will be included in the revised CSRD. |

| Reporting Requirements | |||

| Reporting content and structure | Alignment with the European Sustainability Reporting Standards (ESRS) with sector-specific standards in future years |

Alignment with a streamlined version of the ESRS (not yet published) No sector-specific ESRS standards |

The number of mandatory ESRS datapoints will be substantially reduced and prioritize quantitative datapoints over narrative. |

| Reporting information on the value chain | After a three-year transition period, value chain information should be collected and disclosed where relevant to material sustainability matters | Companies should not obtain information from companies in their value chain who do not fall under the CSRD eligibility requirements beyond disclosure requirements in standards specified for voluntary use (draft VSME standards not yet updated) | The “value chain cap” will ensure spillover effects of the CSRD on companies not in scope will be limited. |

| EU Taxonomy | EU Taxonomy reporting required for companies in scope of the CSRD | Voluntary for companies who fall within the CSRD scope (see large undertaking definition above) AND have ≤ €450 million in net turnover | Companies with less than €450 million in net turnover can “opt in” to EU Taxonomy disclosure. |

| Assurance | Limited assurance with future requirement for reasonable assurance | Limited assurance only | Companies will have a lower cost burden when it comes to assurance of their CSRD Sustainability Statements. |

| Digitization and XBRL tagging |

Require tagging of the CSRD Sustainability Statement to XBRL Taxonomy for ESRS Draft was delayed and published in August 2024 |

No planned XBRL tagging requirements until the Delegated Regulation for marking up the CSRD Sustainability Statement is adopted | No immediate requirement to digitally tag reports. |

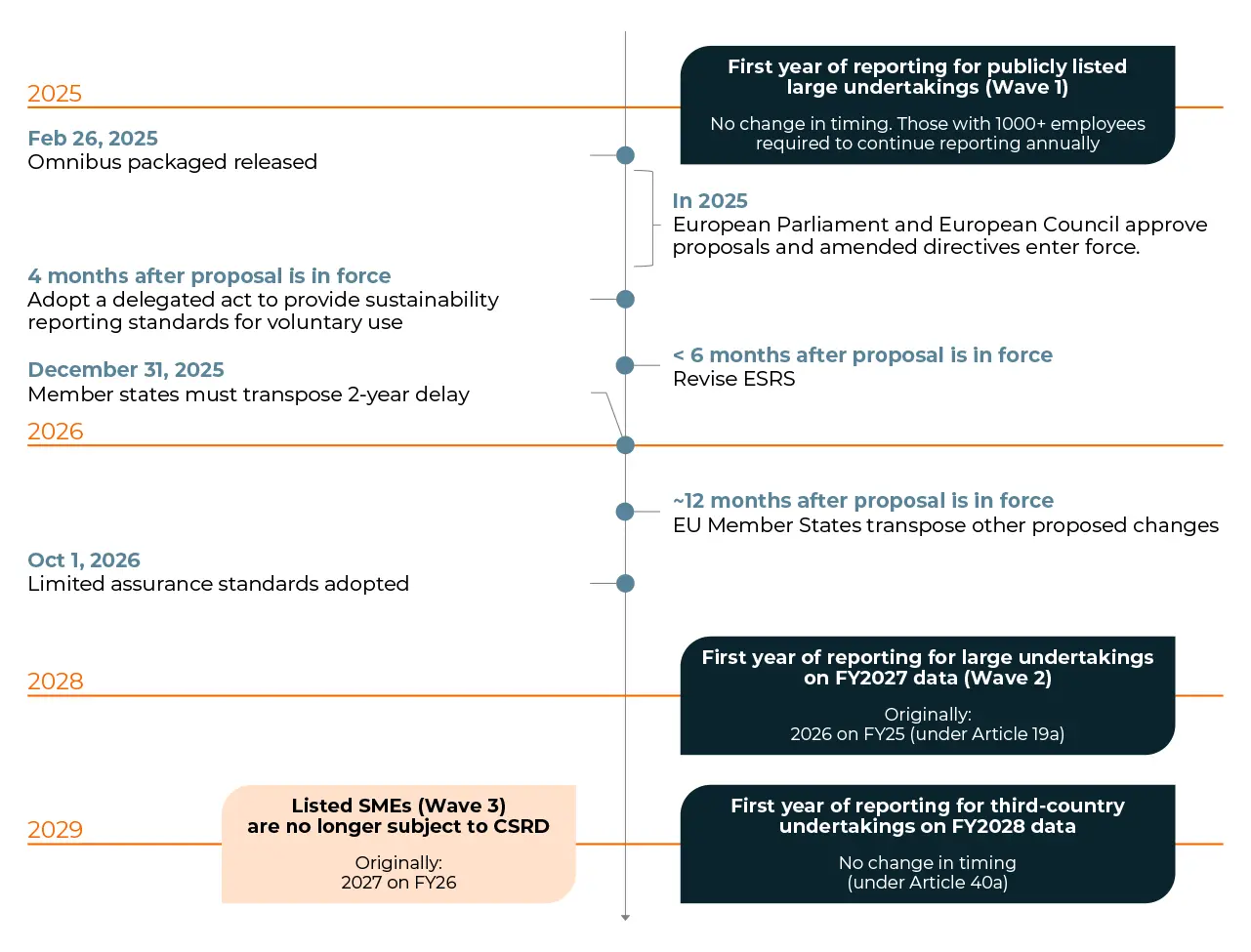

When will these changes take effect?

Although the Omnibus proposal has been released, it will take time before the proposed directives are adopted and transposed into member state law. For those companies still in scope that have not yet reported a sustainability statement, reporting will likely resume in 2028 on fiscal year 2027 data.

Estimated timing is for illustrative purposes and subject to change as more information becomes available.

What does this mean for my company?

Although the Omnibus proposal is still subject to change before final adoption, we recommend that companies use this opportunity to re-evaluate their sustainability reporting approach and strategy.

1. Re-assess eligibility thresholds and determine if you are in-scope for the CSRD

a. As the first year of required reporting has been delayed, consider forecast or growth assumptions that may trigger eligibility in future years.

b. For non-EU companies, re-assess eligibility thresholds for EU subsidiaries, EU branches, and the parent company to confirm whether you are still in scope and determine the first year of reporting required. Companies with a subsidiary having fewer than 1,000 employees initially classified as a Wave 2 reporter may no longer need to report under Articles 19a or 29a but may still be in scope through a branch for reporting under Article 40a.

2. If you are still in scope for the CSRD

a. Continue to improve upon processes and work already invested in preparing for the CSRD

b. Develop a plan to improve and systematize a more efficient process to conduct future CSRD-aligned double materiality assessments. The Omnibus proposal does not indicate changes to the double materiality assessment approach.

c. Continue to collect quantitative metrics relevant to material sustainability matters given that the revised ESRS will prioritize streamlining narrative, non-metric data points.

3. If you are no longer subject to the CSRD

a. Determine how best to leverage work already completed, such as findings from your materiality assessment or ESRS gap assessment, and incorporate it into your sustainability strategy.

b. Continue to develop plans that address your material sustainability matters and incorperate these into your broader strategy by developing policies, implementing actions, and tracking relevant metrics.

c. Revise your approach to standardized sustainability reporting by considering other regulations you are still subject to, aligning with frameworks such as ISSB’s IFRS S1 and S2, and/or applying the Voluntary SME standards drafted by the European Commission in December 2024.

Sodali & Co understands navigating regulatory changes can be challenging.

For many companies, significant effort and investment have gone into preparing for compliance, and these shifts may bring both relief and added complexity.

Simplification of the CSRD is an opportunity to refine and develop a focused, fit-for-purpose approach to addressing sustainability matters that are material to your business and key stakeholders. As the landscape continues to evolve, our global team of sustainability experts is here to support you in a path forward.

Request an exclusive video to learn more

Summary

On February 26, 2025, the European Commission proposed the Omnibus package to streamline the CSRD, CSDDD, and EU Taxonomy regulations. This package, introduced two years after the CSRD’s enforcement, will significantly affect reporting eligibility, timing, and requirements for many companies. The Commission aims to simplify sustainability reporting and due diligence to address economic stagnation and reduce administrative burdens, especially for SMEs. Companies should understand the Omnibus package’s implications for their CSRD preparedness strategy.

Author

Related Reports

From Disclosure to Discipline: Highlights from Our GRESB Fundamentals Webinar

15 July 2026

Climate Reporting in Australia: What the 2026–27 Budget Changes Mean for Your Organization

02 July 2026

AASB S2 in Practice: Early Structural and Governance Insights from Australia’s First Climate Reporters

04 June 2026