Subscribe to stay informed, inspired and involved.

Subscribe

Sign up with your email

On June 30, 2026, the SEC issued a new conditional exemptive order (the “2026 Exemptive Order”) for abbreviated debt tender offers, replacing the SEC’s 2015 no-action letter. The order retains the core five-business-day offering period but eases several of the conditions that shaped the 2015 regime.

The 2026 Exemptive Order significantly expands what issuers can do within the compressed five-business-day timeline, enabling partial repurchases and exchanges, broader investor eligibility and the ability to implement simple majority consent solicitations.

Operational implications for issuers, dealer managers, and legal advisers

As more issuers may now contemplate abbreviated transactions, best-in-class execution becomes increasingly important. Seven practical points stand out:

- Knowing the holder base before launch. With limited time to engage holders once an offer is live, understanding the bondholder population in advance carries more importance than under the 2015 regime. Sodali & Co can assist by undertaking an ‘under the radar’ bondholder identification exercise ahead of launch, where relevant. Our global team of specialists delivers a detailed profile of the holder population, allowing issuers and advisers to plan outreach and anticipate participation before the offer commences.

- Launch timings and a proactive Information Agent. Since announcements must travel faster, with holders having less time to consider and respond to them, launches should occur as early in the day as possible. Any announcements during the offer have a set prescribed window that needs to be adhered to. With a uniquely global platform Sodali’s team is available to handle such announcements and offer launches across multiple platforms whatever the hour.

- Speed of information dissemination is now critical. With participation windows compressed to as little as five business days, the clearing systems, custodian banks, brokers and intermediaries will need to be informed promptly — so that the offer can travel down the ownership chain and be acted on by holders before the respective intermediary, clearing system and market deadlines close in. As part of that process, provision of dedicated project websites, allowing holders access all relevant documentation in one place, becomes key.

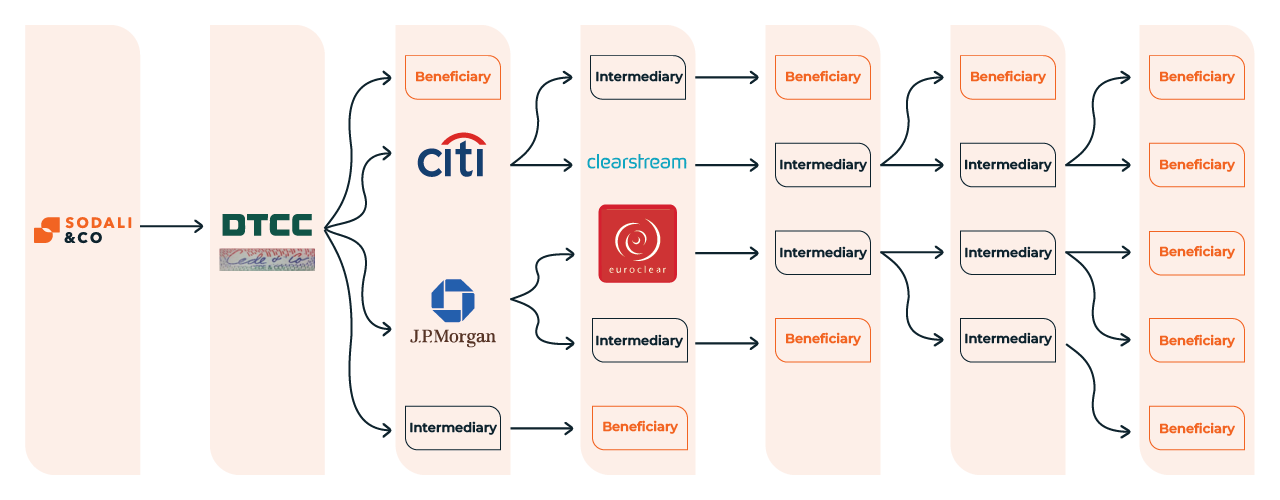

- Reach across the full ownership chain. The Agent needs to be close not only to DTC but also to the specialized depositaries and the international clearing systems, Euroclear and Clearstream. This is particularly critical for Reg S tranches of bonds deposited in DTC held through accounts at Euroclear and Clearstream. Such a set up can be commonplace for non-US issuers, with very significant numbers of bondholders using this custody setup they face an elongated custody chain and are often the first to run out of time to instruct.

Figure: DTC Bonds Typical Custody Chain:

- Combined with that, the 2026 Exemptive Order eliminates the requirement for guaranteed delivery procedures, removing the two-business-day cushion holders previously relied on to complete settlement and participate in the offer. This makes early, proactive engagement even more important for holders further down elongated custody chains. Sodali & Co’s established relationships with Euroclear and Clearstream, as well as their direct participants, help to reduce that risk.

- Real-time visibility on instructions, right up to the deadline. When every hour counts, feedback on participation cannot wait for end-of-day reporting. Through BondWatch, Sodali & Co’s proprietary real-time reporting system, the working group can track bondholder instructions as they come in — a critical advantage in abbreviated offers where time is of the essence[1].

- Broadening investor base participation. While the broadening of the investor base for participation in the offers increases potential demand, the influx of new holders will present its own challenges, requiring a responsive information agent to work alongside issuers and dealer managers to ensure all holders (and their financial intermediaries) are aware of the operational requirements to validly participate in the offer.

As abbreviated liability management transactions into the US become a more versatile tool under the 2026 Exemptive Order, the agents best placed to support clients will be those with the market relationships, global reach, superior operational infrastructure, and teams able to move at speed.

Sodali & Co would welcome the opportunity to discuss how we can support your next LM transaction. Learn more about our Global Debt Services capabilities.

Summary

The SEC’s 2026 Exemptive Order updates and expands the 2015 framework for abbreviated debt tender offers, maintaining a five-business-day offer period while enabling partial repurchases, broader investor participation, and majority consent solicitations, with operational emphasis on early holder identification, rapid information dissemination, global custody reach, elimination of guaranteed delivery, real-time instruction visibility, and enhanced agent support for diverse investor bases to ensure efficient execution of liability management transactionsin the US.

Author

Related Reports